Chapter 1:

Why Cash is King

The Reality of the Business World

It’s easy to get lost in the allure of huge revenues and profits. But, underneath these headline-grabbing numbers lies a fundamental truth every seasoned businessperson knows: Cash is King.

It’s not just a catchy phrase; it’s the underpinning of successful business management. While revenues and profits indicate a company’s potential or performance on paper, cash represents its actual ability to cover expenses, pay employees, invest in growth, and withstand downturns.

The Power of Liquidity

Liquidity is not just about having spare cash in hand; it’s about the freedom and options it provides. A robust liquidity position means having the ability to absorb unexpected expenses and uncertainties. When unforeseen challenges like the COVID-19 pandemic strike, those with a sound cash flow forecast and a solid cash flow cycle are better positioned to weather the storm. In many ways, the pandemic acted as a litmus test, distinguishing businesses based on their cash readiness.

Effective cash management doesn’t just act as a shield; it’s also a sword. It enables businesses to capitalise on opportunities that others, with business cash flow issues, might overlook. Investors who evaluate a business often bypass the “vanity metrics” such as revenue size. They focus instead on the cash flow forecast and actual cash flows of the enterprise, knowing that positive cash flow often dictates a company’s true health and potential.

The Hard Truth: Statistics Don’t Lie

The significance of cash management is highlighted in a stark reality:

82% of business failures in Australia are attributed to poor and irregular cash flow.

Moreover, a startling 44% of firms lean on business credit cards and other finance options for day-to-day operations. These numbers underscore a critical need for businesses, especially small and medium-sized enterprises, to prioritize their cash flow forecast and tackle cash flow issues proactively.

The Ultimate Mantra

“Revenue is vanity, profit is sanity, and cash is king.”

While robust revenue figures might earn admiration, and profit indicates sound business operations, neither guarantees survival. It’s the tangible cash in the bank that settles bills, meets emergencies, and sows seeds for future growth. It’s cash that truly reigns supreme in the realm of business.

Chapter 2:

Where Did My Profits Go?

At the end of the year, many business owners are left wondering, “Where did my profits go?” despite seeing a positive net income on their profit and loss statement. The answer lies in understanding the importance of working capital and its influence on cash inflows and outflows. Only when you understand this, can you craft an effective cash flow plan.

This video takes a look at the following:

- Even with a solid gross profit, subtle changes in costs or working capital metrics can shift your cash flow.

- It’s not just about revenue and operating profit. Consider the impact of accounts receivable, inventory days, and accounts payable on your bottom line.

- Balance sheets tell a deeper story: sometimes, increasing profitability or securing a good deal might result in less immediate cash.

Chapter 3:

Understanding Your Working Capital?

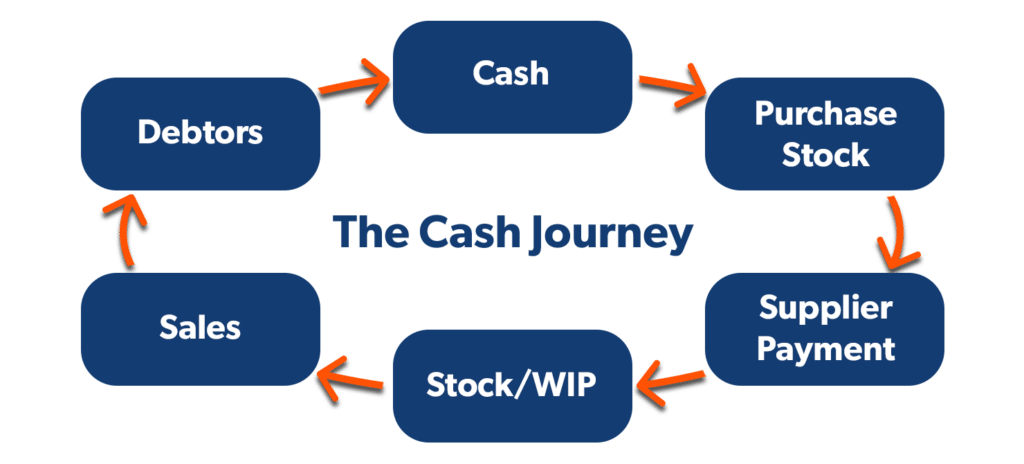

Let’s take things a step further and have a look at what’s involved in working capital. This image shows us the flow of cash within your business:

Simply put, you’re using your cash to purchase stock, pay suppliers, sell the stock, and get paid by debtors. So, your cash goes from you to your suppliers, and then you get it back from your customers.

Pretty straightforward right? BUT the length and what’s involved in that cycle can have an enormous impact on how successful your business is.

Let’s look at each of those metrics, how you calculate them, and then some strategies to improve them.

Metrics in the Working Capital Cycle

Debtor Days:

A measure of the average number of days it takes a company to collect payment after a sale has been made. It’s a key metric to gauge the efficiency of your accounts receivable department.

A higher number means that it’s taking longer for the company to collect money from its customers. This could be due to lax credit policies or issues with the quality of goods/services. A higher debtor days might strain a company’s cash flows.

Formula: (Total Debtors Balance/ Total Annual Revenue) x 365

A company called Massive Dynamic has $137,000 sitting in debtors, and a turnover of $1,000,000 per year.

Debtor Days = (137,000/1,000,000) x 365 = 50

Following the above formula, they have 50 debtor days.

Creditor Days:

Indicates how long a company takes on average to pay its suppliers.

A higher number means that the company is taking longer to pay its suppliers, which could be beneficial as it means they are keeping cash in the business for longer. However, if it’s too high, it may strain relationships with suppliers or indicate cash flow problems.

Formula: (Creditors Balance/ Annual COGS) x 365

Massive Dynamic has a margin of 20%, so it’s annual COGS is $800,000.

They also have $76,700 sitting in creditors.

Creditor Days = (76,700/800,000) x 365 = 35

So Massive Dynamic has 35 creditor days sitting on the balance sheet at any time.

Inventory Days:

Represents the number of days, on average, goods remain in inventory before being sold.

A higher number might indicate slow-moving inventory or overstocking, while a low number could mean good inventory management or potentially understocking, which might lead to missed sales opportunities.

Formula: (Inventory Balance/ Annual COGS) x 365

Massive Dynamic has an inventory balance of $263,000

Inventory Days = (76,700/800,000) x 365 = 120

Therefore we’ve got 120 inventory days.

Working Capital Days:

The combination of all the above. It provides an overall view of the efficiency of a company’s operations and cash management.

A higher number indicates that cash is tied up in operations for a longer period, which might strain the company’s liquidity.

Formula: Inventory Days + Debtor Days – Creditor Days

Working Capital Days = 120+50-35 = 135

Massive Dynamic has a long cycle in terms of converting its operations into cash, which could indicate potential liquidity challenges, especially with a relatively high debtor and inventory days.

Our main goal then is to shorten the cycle so that the business recoups its investments along with the profit margin more quickly. Remember that each business is unique, so our advice here is general, but here’s a couple of things that might work in your business.

Reducing Debtor Days

Every business should have a robust accounts receivable policy that the accounts team understands. This includes understanding your credit terms, knowing who you extend credit to, and having a clear strategy for addressing outstanding payments. It’s essential to document this policy and ensure it’s adhered to.

Businesses should also perform credit checks, especially when taking on significant new accounts. This ensures the client has a track record that aligns with the credit terms you’re offering. From a strategic perspective, consider revising your pricing structure and payment schedules. Think about whether you can ask for down payments or adjust the frequency of payments for more extensive projects.

While invoice financing is an option, it’s not always ideal. It might temporarily address cash flow issues, but if poor cash flow is symptomatic of deeper problems, then invoice financing just masks the real issue, potentially worsening it later.

A critical note: avoid offering early payment discounts. They’re one of the most costly financing methods available.

Increasing Creditor Days

This can be a bit more challenging. The most apparent strategy is to negotiate payment terms, at the very least, by raising the question.

If a supplier refuses to extend payment terms and there’s an alternative product with better terms that could positively impact your cash conversion cycle, it may be worth considering other suppliers. We’ve observed that clients leveraging their spending data during negotiations is particularly effective.

For instance, if you’re a significant customer to a supplier, you can present data like: “Our expenditure with you has grown from $40,000 in the first year to $400,000 in the second, reaching a million dollars in the third year. Here’s our projected spending for the next two years.” Presenting this visually to highlight your importance to them can enhance your negotiating position.

Lastly, it’s crucial to treat suppliers as essential partners. Regular communication, just like with any key stakeholder or customer, ensures they understand your business strategy and future directions. A solid relationship with them provides leverage when discussing terms or seeking support.

Reducing Inventory Days

The approach to this will vary based on the type of products you sell and stock.

One thing is crucial regardless of what you’re selling: active inventory management. You need accurate inventory tracking and the capability to forecast based on your sales pipeline. You don’t want a thumb-in-the-wind approach to securing inventory; it should be based on sales.

You also need a strategy for addressing slow-moving or obsolete items and how to get rid of them. This could involve bundling them with popular products, selling them through an online store, or under a sub-brand.

Analyse what you’re stocking and ensure you’re not stocking anything you don’t need to. Look at the numbers, analyse what’s actually selling and then be honest with yourself about what range is required.

Chapter 4:

The 3F Approach (Forecasting, Funding, Focus)

Forecasting

Forecasting is the backbone of good cash flow management. Without forecasting, you can’t expect to manage your cash effectively.

There are two types of cashflow forecasts you need in your business;

Long Term: Your long-term forecast is directly connected to your annual P & L forecast and would typically be for a period of twelve months. It will give you a big-picture view of your cash flow for the year ahead and help guide your strategic decisions.

Short Term: To effectively manage your cashflow week to week, you need a short-term three-month forecast, or twelve/thirteen weeks. This allows you to get much closer to your operational requirements.

13 Week Cashflow Forecast

There are three golden rules to remember with your cash flow forecast.

- Keep it alive: Your forecast will be out of date almost immediately, so you need to keep it up to date. Update it once a week and roll it forward every month.

- Success, not perfection: Make a start and refine it as you go. Don’t put too much detail in your forecast. Keep it high level. Get the big numbers right, and don’t sweat the small stuff.

- Stay close to the numbers: Someone must take ownership of the forecast. It’s difficult for someone to manage externally. You can’t just expect to outsource effective forecasting to your accountant. Someone needs to be intimate with what is happening.

Funding

Now tight cash flow is not always a bad thing, within reason. It can make you more diligent and disciplined in managing your cash flow and help cut down on cash wastage. But when cash flow is too tight, it’s restrictive. It will limit your options and hinder your growth.

So you need to ensure you’re not starving your business of funding. A good relationship with your bank manager is critical because a crisis is no time to introduce yourself. You’ll be on the back foot. Unfortunately, when things are tight and heading into crisis mode, this is the time when most business owners start looking for additional funding. When you fall into this trap, it effectively means you’re asking the bank for help when they’re least likely to provide it.

So get onto the front foot. How long is it since you requested a funding review? Or asked about alternative funding or lower interest rates and fees? How about approaching another bank or lender to see what they can offer? You need to treat your bank as a supplier – you need to have a good relationship and negotiate well.

Focus

It may seem a little obvious, but if you want better cashflow, you need to act like it. This means spending time and focusing on what is required to improve.

Start with the low-hanging fruit first off. You will be able to identify these things quickly enough. It may be diligent follow-up of some overdue debts. It may be turning slow-moving stock into cash or talking to some suppliers to negotiate extended payment terms.

But the short-term fixes don’t fix your structural cashflow problems, so you need to spend more time, more regular focused time, to implement structural improvement.

For the most part, the best use of your time is in improving your cash conversion cycle, so your working capital. Monitor your debtor days, inventory days, and creditor days. Spend some time, get it right and figure out how you can improve? Review your fixed costs. A dollar saved is a dollar earned, which is a dollar extra in cash—then funding. Spend some time, focus on it. Do you have the proper facilities? Can your funding mix be improved?

Just invest some time to focus on improving the fundamentals of your cash flow.

So that’s the 3F Framework – Forecasting, Funding and Focus. It is a simple approach that works and can pay dividends in your business if you set aside some time to work through it.

Chapter 5:

How to Survive a Cash Flow Crisis

Cashflow crises can happen to any business, big or small. It can be stressful, and overwhelming and can lead to bad decision-making. However, there are steps you can take to overcome it. Here are some key steps to help you survive a cash flow crisis.

1. Don’t Panic

The first step when facing a cash flow crisis is to avoid panicking. Panicking can lead to making hasty decisions without considering the facts. It’s important to take a deep breath, step back and assess the situation.

2. Get the Facts

The next step is to get the facts. Speak to your accountant and get a clear understanding of your financial situation. Find out exactly who owes you money, when they’ll pay, who you owe money to and when it’s due. Make a list of all your short-term cash commitments, including overheads, salaries, and other expenses. Also, determine the amount of cash available to you from equity, funds outside the business or any credit facilities available through your bank.

3. Communicate, Communicate, Communicate

Communication is key when dealing with a cash flow crisis. Communicate with your team, especially the management team, and make sure they understand the situation. Communicate with your customers and make sure they know when you expect payment. Also, communicate with your suppliers and try to establish a payment plan that works for both parties. Over-communication is better than under-communication in these situations.

4. Tighten the Screws

When you’re facing a cash flow crisis, it’s important to tighten the screws on your finances. Focus on managing your accounts receivable and tighten the screws on inventory management. Identify what is moving and what isn’t and manage your inventory accordingly. Additionally, go through your overheads line by line and identify any unnecessary expenses. Any money going out in the business should be to generate more money coming in.

5. Make the Tough Decisions

If you’re in a cash flow crisis, it may be necessary to make tough decisions. If you need to, establish a hit list of non-essential expenses that can be cut if needed. Take the emotion out of the situation and focus on the facts and data. If necessary, be prepared to turn off the tap to some areas that aren’t delivering, whether that’s departments or people.

Chapter 6:

Your Cash Flow Action Plan

The 7 Point Cash Flow Action Plan brings everything together and provides a systematic approach to managing and enhancing cash flow, ensuring both financial stability and sustainable growth for businesses of all sizes.

1. Understanding the Cash Conversion Cycle (CCC)

The Cash Conversion Cycle (CCC) is the duration between when you spend money (on inventory or raw materials) and when you collect money from sales of products/services. It’s crucial to understand your business’s CCC to efficiently manage and improve cash flow.

- Action Steps:

- Calculate your current CCC.

2. Short-term Cash Flow Forecasting

A projection of your business’s cash inflows and outflows over a short period (e.g., weekly or monthly).

- Action Steps:

- Utilise available templates or software to start forecasting.

- Update forecasts regularly to reflect the actual situation.

- Analyse variances and adjust strategies accordingly.

3. Bank Relationship and Financing Options

Engaging with your bank to discuss financial obligations and explore financing options.

- Action Steps:

- Schedule regular meetings with your bank manager.

- Understand all available loan and credit options.

- Ensure you have a buffer or overdraft facility for emergencies.

4. Alternative Funding Sources

Exploring non-traditional methods of securing funds.

- Action Steps:

- Research peer-to-peer lending, crowdfunding, venture capital, and other non-bank options.

- Compare interest rates, terms, and conditions.

- Align funding sources with your business’s growth strategy and needs.

5. Debtor Management Process Review

A review of how you manage those who owe you money to ensure timely payment.

- Action Steps:

- Implement a clear invoicing system.

- Regularly review outstanding accounts.

- Set up automated reminders for late payments.

6. Inventory Analysis

A deep dive into your inventory to identify profitable products and optimize stock levels.

- Action Steps:

- Conduct regular inventory checks.

- Implement a Just-In-Time (JIT) inventory system if feasible.

- Discontinue low-profit products and focus on high-margin items.

7. Supplier Payment Terms Negotiation

Working with suppliers to establish favorable payment terms.

- Action Steps:

- Review current supplier contracts and terms.

- Negotiate longer payment periods or discounts for early payments.

- Build strong relationships with key suppliers for leverage.

By consistently applying this 7-Point Cash Flow Action Plan, businesses can not only improve their cash flow but also set the stage for sustainable growth and stability.

How Can Quantum Advisory Help?

Managing your cash flow alone can be tricky, so let our experts guide you. We’ll do a complete analysis of your cash flow and identify the areas for improvement, then give you actionable strategies to make it happen.

Vypa Workwear partnered with Quantum in 2022. Within the first quarter of working with them, the team at Quantum was able to reduce their debtor days from 57 to 22.

Partnering with Quantum Advisory allows you to focus on what you do best – running your business – while leaving the financial aspects in capable hands.